Name Number of Shares Total Cost Total Fair Value

Tornado Inc. 800 $14,000 $15,600

Tsunami Corp. 1,250 31,250 35,000

Typhoon Corp. 2,140 43,870 42,800

Total $89,120 $93,400

On June 12, 2015, Hurricane purchased 1,450 shares of Rogue Wave Inc. at $45 per share plus a $100 brokerage fee.

a. Provide the journal entries to record the following:

1. The adjustment of the available-for-sale security portfolio to fair value on December 31, 2014.

2. The June 12, 2015, purchase of Rogue Wave Inc. stock.

b. How are unrealized gains and losses treated differently for available-for-sale securities than for trading securities?

Answer:

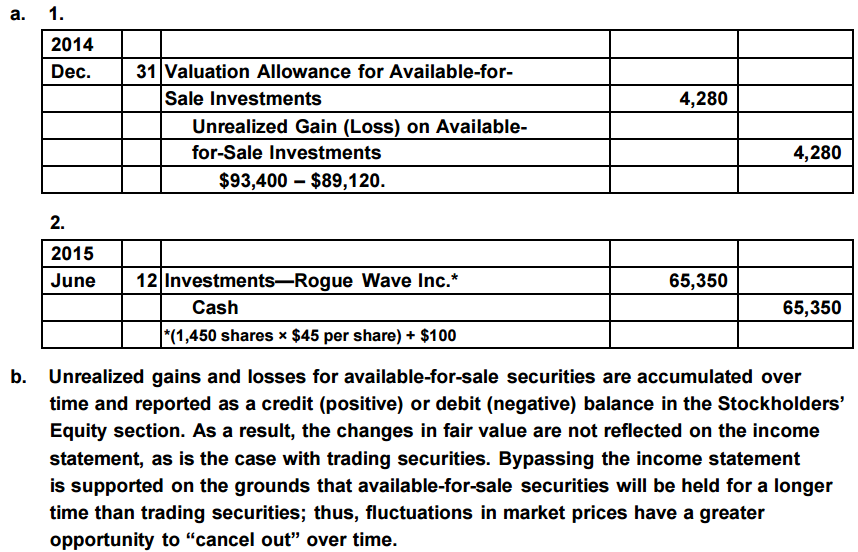

a. 1.

2014

Dec. 31 Valuation Allowance for Available-forSale

Investments 4,280

Unrealized Gain (Loss) on Availablefor-Sale

Investments 4,280

$93,400 – $89,120.

2.

2015

June 12 Investments—Rogue Wave Inc.* 65,350

Cash 65,350

*(1,450 shares × $45 per share) + $100

b. Unrealized gains and losses for available-for-sale securities are accumulated over

time and reported as a credit (positive) or debit (negative) balance in the Stockholders’

Equity section. As a result, the changes in fair value are not reflected on the income

statement, as is the case with trading securities. Bypassing the income statement

is supported on the grounds that available-for-sale securities will be held for a longer

time than trading securities; thus, fluctuations in market prices have a greater

opportunity to “cancel out” over time.