Actual: Variable factory overhead $262,000

Fixed factory overhead 90,000

Standard: 14,000 hrs. at $25 350,000

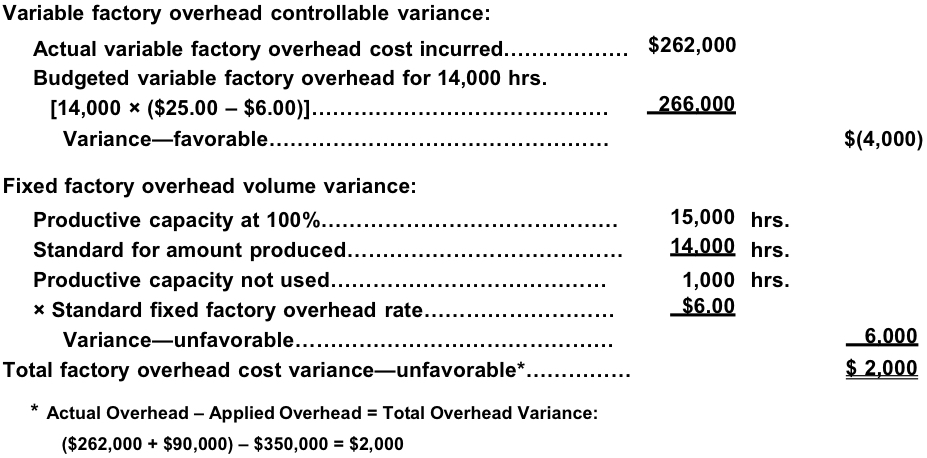

If productive capacity of 100% was 15,000 hours and the total factory overhead cost budgeted at the level of 14,000 standard hours was $356,000, determine the variable factory overhead controllable variance, fixed factory overhead volume variance, and total factory overhead cost variance. The fixed factory overhead rate was $6.00 per hour.

Answer:

Variable factory overhead controllable variance:

Actual variable factory overhead cost incurred……………… $262,000

Budgeted variable factory overhead for 14,000 hrs.

[14,000 × ($25.00 – $6.00)]…………………………………… 266,000

Variance—favorable………………………………………… $(4,000)

Fixed factory overhead volume variance:

Productive capacity at 100%…………………………………… 15,000

Standard for amount produced………………………………… 14,000 hrs.

Productive capacity not used………………………………… 1,000 hrs.

× Standard fixed factory overhead rate………………………

Variance—unfavorable………………………………………

Total factory overhead cost variance—unfavorable*…………… $ 2,000

* Actual Overhead – Applied Overhead = Total Overhead Variance:

($262,000 + $90,000) – $350,000 = $2,000

Alternative Computation of Overhead Variances

Factory Overhead

Actual costs 352,000 Applied costs 350,000

Balance (underapplied) 2,000

Budgeted Factory

Overhead for Amount

Produced

$352,000 Variable cost [14,000 × ($25.00 – $6.00)]……… $266,000 $350,000

Fixed cost………………………………………… 90,000

Total………………………………………………… $356,000

–$4,000 F $6,000 U

Controllable Volume

Variance Variance

$2,000 U

Total Factory Overhead

Cost Variance